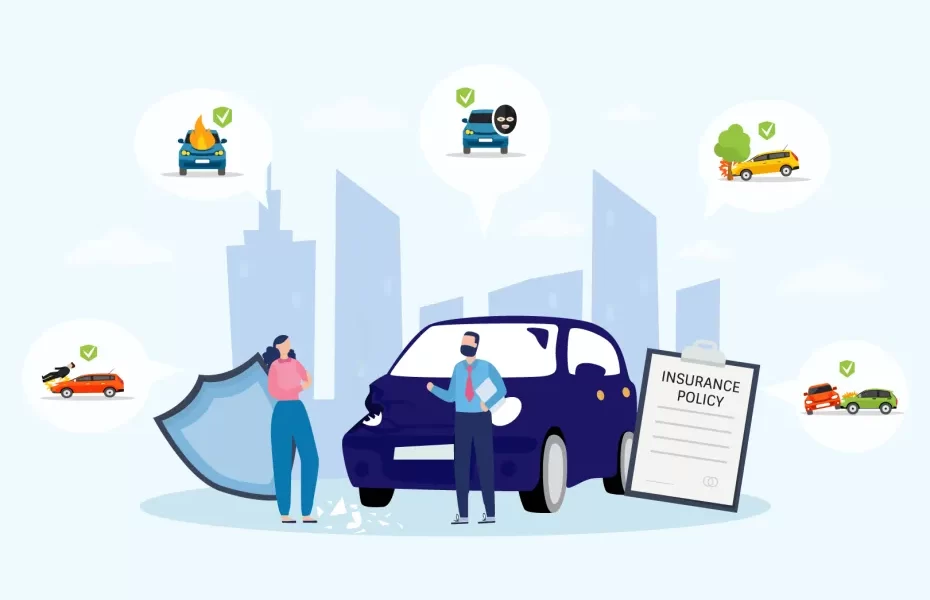

In an ever-evolving world filled with unpredictability, safeguarding your financial interests remains of utmost importance. This principle is exemplified when considering your automobile, a substantial investment for most individuals. While conventional auto insurance might already be in place, there exists a relatively lesser-known yet equally crucial form of protection, known as gap insurance. This article aims to explore the nuances of gap insurance, elucidating its purpose and highlighting its significance for all vehicle owners and lessees.

Read more.. Less than ₹50 Stock Surges with a 20% Upper Circuit

Read more.. the Art of Securing an Easy Loan: Top Tips for Success

Understanding the Gap

Gap insurance, also known as Guaranteed Asset Protection insurance, serves as a crucial shield by bridging the financial chasm between your vehicle’s depreciated actual cash value (ACV) and the outstanding balance on your auto loan or lease. This indispensable coverage comes to the rescue when the unexpected occurs, such as theft or a catastrophic accident, as your regular auto insurance policy often falls short, leaving you responsible for the substantial disparity between ACV and your financial obligations.

Read more.. Why is a Credit Score most Important for Us?

Read more.. YES Bank Shares in Focus: JC Flowers ARC & Chief Risk News

How Gap Insurance Works

To better understand gap insurance, consider a scenario:

Picture this scenario: You invest in a shiny, new $30,000 car, securing an auto loan to make it happen. But, just a few months down the road, a major accident leaves your car completely totaled. Now, your regular auto insurance evaluates your vehicle’s Actual Cash Value (ACV), likely around $25,000 due to depreciation. Yet, you’re left with a remaining auto loan balance of $28,000, highlighting the crucial role of gap insurance—a $3,000 lifesaver in this situation.

Gap insurance covers that $3,000 gap, ensuring that you don’t have to pay out of pocket for a car that you no longer possess. This invaluable coverage can prevent you from experiencing financial hardship during an already challenging time.

Who Needs Gap Insurance?

Gap insurance is particularly beneficial for certain individuals:

1. New Car Owners: Gap insurance is highly recommended for those who purchase brand-new vehicles, as the depreciation rate is steepest in the first few years. If your car is totaled during this period, you could be left with a significant financial burden without gap coverage.

2. Leaseholders: If you’re leasing a vehicle, gap insurance is often required by the leasing company. It ensures that you’re not responsible for the gap between the ACV and the remaining lease balance if an accident occurs.

3. Low Down Payment: If you made a small down payment or financed additional costs like taxes and fees, the gap between your loan balance and your car’s value can be substantial. Gap insurance can provide peace of mind in such cases.

4. Long-Term Loans: If you’ve taken out a long-term auto loan (typically more than 60 months), you’ll benefit from gap insurance, as your car’s depreciation will outpace your loan balance reduction for an extended period.

Conclusion

Amidst the ever-shifting landscape of financial uncertainties, gap insurance emerges as an indispensable shield for safeguarding your automotive investment. It might not be a universal necessity, but it emerges as a wise decision for individuals acquiring new vehicles, leasing automobiles, providing minimal initial payments, or choosing extended loan terms. By effectively bridging the chasm between your auto loan balance and your vehicle’s real-world market worth, gap insurance guarantees that you remain insulated from financial turmoil should the unforeseen strike. In the realm of safeguarding your investments, knowledge and preparation serve as your most reliable companions, and gap insurance stands as a formidable asset within your toolkit.